What is Behind the Blockchain Doomsday Calls?

- By Ceecee Wong

- February 25, 2019

Blockchain may have ridden the technology buzz train along with AI, IoT, and Big Data in 2018, but it emerged with a most significant dose of skepticism.

Some analysts and media observers have started tolling the bells of doom. Forbes, Wired and Financial Post are some of the famous detractors.

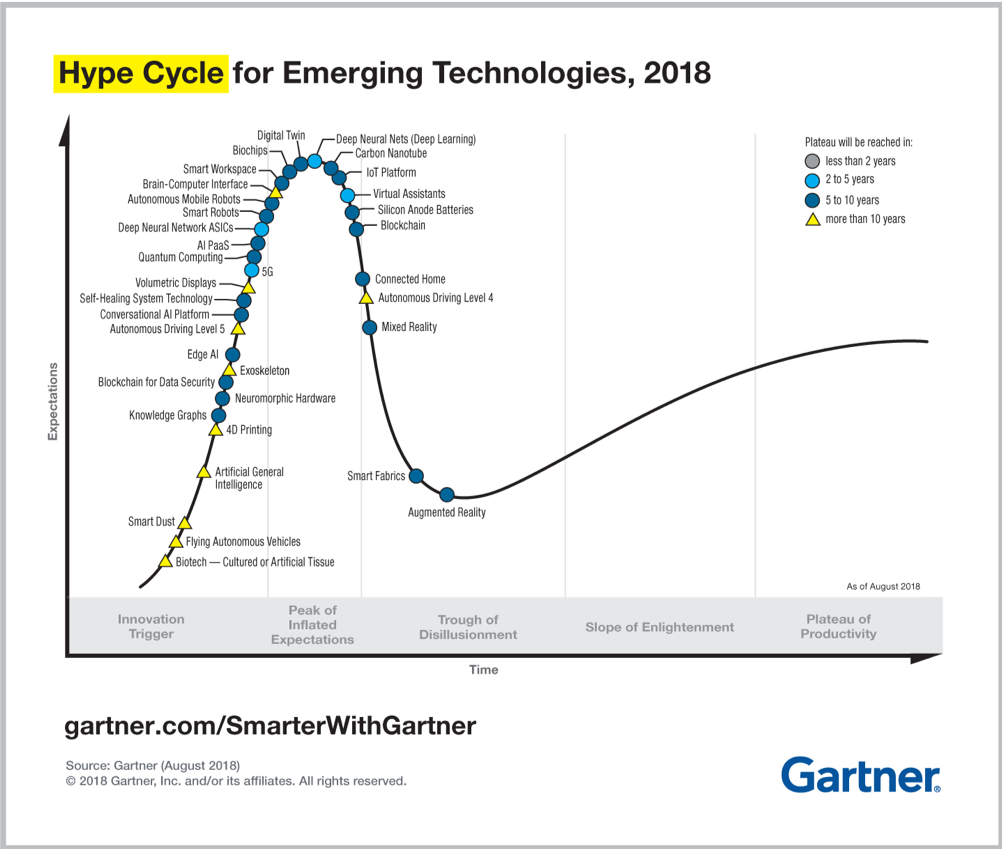

According to Gartner's Hype Cycle for Emerging Technologies (see Diagram 1), blockchain has come out of its Peak of Inflated Expectations and is entering the Trough of Disillusionment. From a technology lifecycle perspective, it is not surprising then that the hype is gone. This is clear for both blockchain adherents and adversaries.

However, the raging debate now is whether the technology still merits the kind of attention and investment it will need to move on to mass adoption.

Blockchain's Historical Context

It is essential to understand that the initial hype of blockchain was inextricably tied to the anarchist overtones of early adopters.

When Satoshi Nakamoto first put the infant technology under the spotlight with the invention of Bitcoin, its early success could largely be attributed to crypto-anarchist cypherpunks. They cherished and nourished the new alternative and experimental monetary system built on blockchain technology that was a direct challenge to the established fiat money regime.

Fast forward ten years later, and we see the potentially game-changing technology extended to industries from financial and accounting services to healthcare, agriculture and the public sector. It shows that despite the highly technical and abstract nature of this space, the technology has managed to cross, or is at least in the process of crossing, the hurdle to enterprise adoption, surely no easy feat in itself. It is worthy to note that regulators have also since moved from obstruction to deliberation, conversation and adaptation.

So why decry it now?

Confusion, Dilemma and Competition

One of the misguided reasons for the disparaging criticism hurled at the technology is invariably tied to the dismal performance of the cryptocurrency market in 2018.

According to CNBC, the total market capitalization of all cryptocurrencies fell to around USD 138.6 billion down more than 80 percent since its January 2018 peak. The negative sentiments surrounding questionable ICO (Initial Coin Offering) projects have often been confused with the merits of the underlying technology, and it is imperative to separate the two.

What's more important to note, as pointed out in the McKinsey article Blockchain's Occam Problem is that in implementing blockchain technology, “the payments industry faces a classic innovator’s dilemma: incumbents understand that investing in disruption, and the likely resulting rise in customer expectations for faster, easier, and cheaper services, may lead to cannibalization of their own revenues.”

Financial institutions already realize that faster, easier and cheaper services do not translate to rising revenues. Moreover, deploying blockchain demands that enterprises be willing to embrace decentralization in their business models and processes, which is not necessarily a one-solution-fits-all for all.

Interestingly, Gartner “anticipated that through 2018, 85 percent of projects with ‘blockchain’ in their titles would deliver business value without actually using a blockchain.”

Besides existing technology solutions, McKinsey's article also cites another reason for the lack of current progress in blockchain - the emergence of competing technologies. For example, SWIFT's global payments innovation (GPI) initiative, a cross-border payment solution that promises higher transaction speeds and increased transparency.

Why Blockchain Will Still Matter

Conceptually blockchain has the potential to redefine economies and industries. What the many failed POC's (proofs-of-concept) have taught us is that we must exercise discernment and realize that not every business or economic-social problem requires blockchain technology as a solution.

We must first recognize that blockchain is a specialized technology well-suited to providing solutions for handling specific types of use cases, especially where issues of immutability, transparency, authenticity, decentralization and governance are of paramount importance.

Data security, data integration and the democratization of data accessibility in supply chains, identity management and the sharing of public records are valuable applications of blockchain technology as it enables transparency, automation and collaboration in a variety of industries such as healthcare, shipping, insurance and government amongst others.

In government, the most transformational impact will be seen in uses such as identities, voting, public records and citizen transactions. Already, governments like Estonia have used blockchain technology in production since 2012 and 99 percent of its public services are online 24/7, while Ukraine has explored blockchain for regional elections and Brazil is in the process of using blockchain-enabled voting to conduct national referenda.

The increasing acceptance of Bitcoin and other blockchain-powered cryptocurrencies recently as mainstream financial instruments has also challenged the traditional economic milieu in irrevocable ways, another clear indication that blockchain is here to stay.

Gartner warns that while “re-engineering businesses to the extent that blockchain envisages will take time... that doesn’t mean it won’t happen and the extent of that change on businesses, industries and society will be enormous.” Predicting that “blockchain’s business value-add will grow to slightly over USD 360 billion by 2026, then surge to more than USD 3.1 trillion by 2030” is a clear indication that businesses need to “start planning, to capture future value as well as mitigating competitive threats, from, for example, new decentralized operating and distributed business models.”

It Comes Down to Scale, Costs

Perhaps the most significant hurdle to mass adoption of blockchain technology at this stage is scale and high transaction costs.

While there are no overnight solutions to such obstacles and we need to recognize that new technologies take time, especially something as foundational as blockchain, the good news is that with lessons continually being learned and applied, developers of distributed ledger projects continue to churn out solutions to address these challenges.

Stellar and Ripple have exciting partnerships, including IBM's cross-border payments partnership with Stellar. Some financial services are already using Ripple, like Cuallix, MercuryFX, IDT, Euro Exim Bank and Catalyst Corporate Federal Credit Union, with many more in the pipeline.

Better and faster blockchains with significantly lower transaction costs are currently being built for the near future on Lightning Network, Raiden Network, Trinity and an increasing number of newer blockchains.

We would do well to remember that in the early 90s, many of these types of obstacles confronted the internet and we wondered whether such complicated and initially costly technology would ever scale to mass adoption.

Look at us now.