4 Trends Driving Record Investment in Technology at Global Banks

- By Qin Li, Tamr

- October 27, 2021

While writing the piece, I came across interesting trends about the pace of technical investment at global banks.

Consider this statement by Deloitte. In their 2021 Banking and Capital Markets Outlook, Deloitte noted that COVID-19 “not only accelerated digital adoption, but it has also been a litmus test for banks’ digital infrastructures. Institutions that made strategic investments in technology came out stronger, but laggards may still be able to leapfrog if they take swift action to accelerate tech modernization. Across the board, digital inertia has faded, and more banks are pursuing technology-driven transformation.”

While each bank is uniquely positioned — there are commonalities among their technical investments.

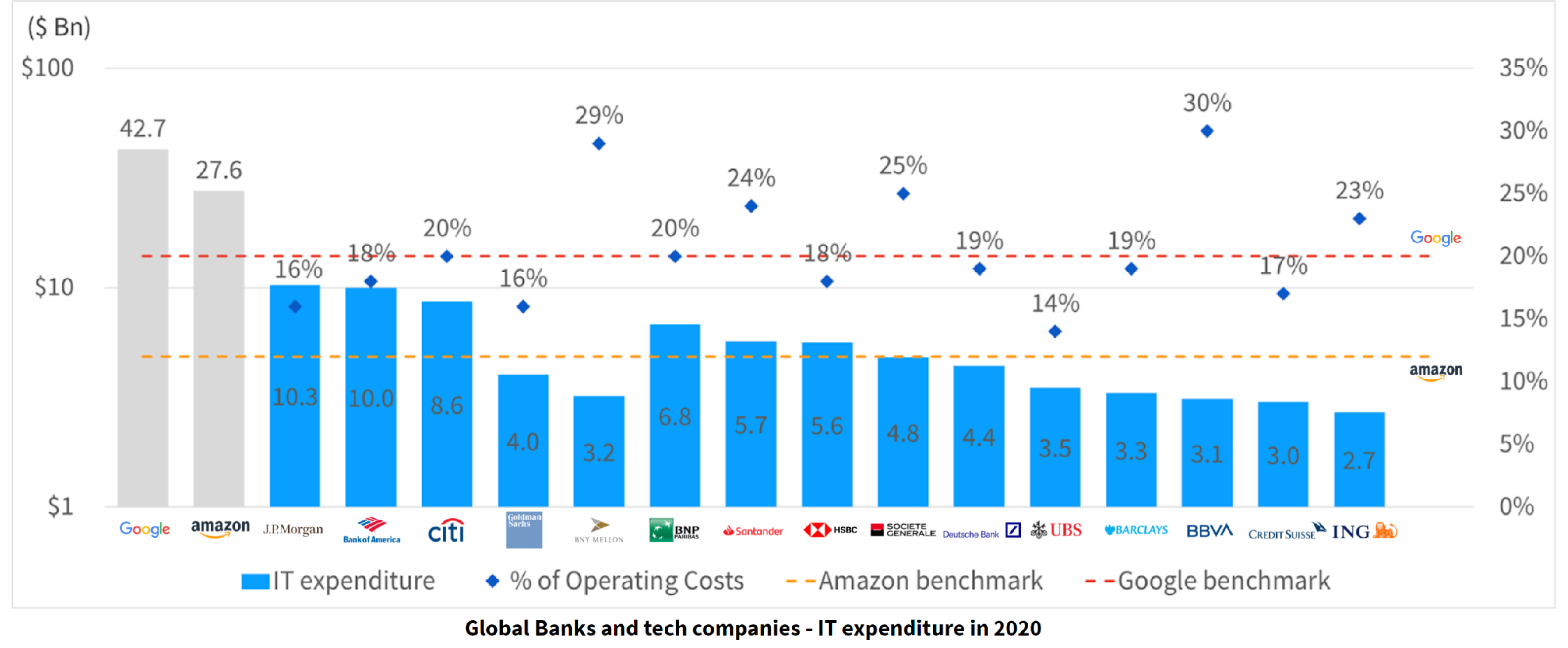

Trend One: Global Banks are outspending tech giants

A JPMorgan Report in June 2021 estimated that Global Banks would continue to invest in efforts to transform their IT to an extent that can match or exceed IT investments by technology giants such as Google and Amazon (figure 1). According to this report, Google and Amazon are spending USD42.7bn and $27.6bn on IT expenditure, respectively. That’s much higher than any financial institution in the world. But if we adjust for the overall operating costs of these companies, Google is spending 20% of their total operating costs while Amazon is spending 12%. In comparison, some banks such as BBVA and BNY Mellon are spending as much as 30% of their total operating costs on IT.

This should play to the advantage of scale players, which have the revenue base to support these platform investments and still generate an acceptable RoE for the shareholders. Of course, the definition of technology expenses may not be comparable across companies. For example, factors such as differences in technology investments (amortization vs. capitalization) or differences between “run the bank costs” vs. “change the bank costs” might change the detailed numbers. But undoubtedly, wisely spent technology investment will be an increasingly important differentiator between banks of all sizes, and the role of technology is increasingly going to be a key determinant of market share winners and losers.

Trend Two: Consolidating technology platforms

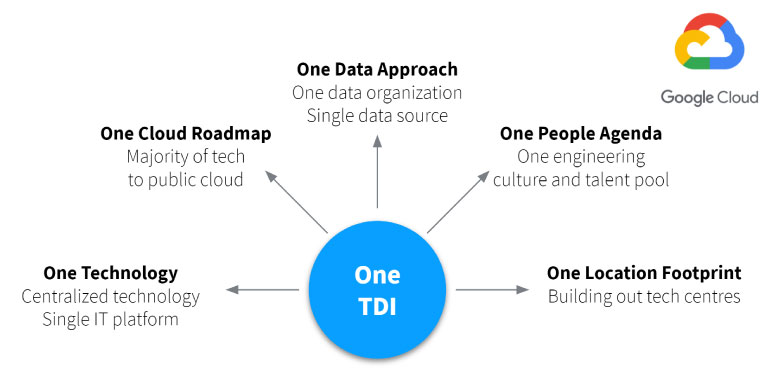

Global banks are not just rethinking about investing in technology but also reorganizing how they operate with technology. For example, in December 2020, Deutsche Bank did a deep dive into their One TDI (Tech, Data & Innovation) Strategy, where they signed a strategic partnership with Google Cloud and consolidated all their technology divisions for benefits such as enhanced efficiency, elasticity, and resilience; faster time to market; and access to best in class technology.

As a measurement for success, they listed: retiring duplicated and outdated applications, rolling out a single source for reference data, and improving productivity through robotic process automation. As far as we know, one technology division for global banks might be a new technology trend that many will follow.

Digitalization and automation have been an ongoing trend as well amongst banks – as more processes are automated and manual intervention reduced/eliminated.

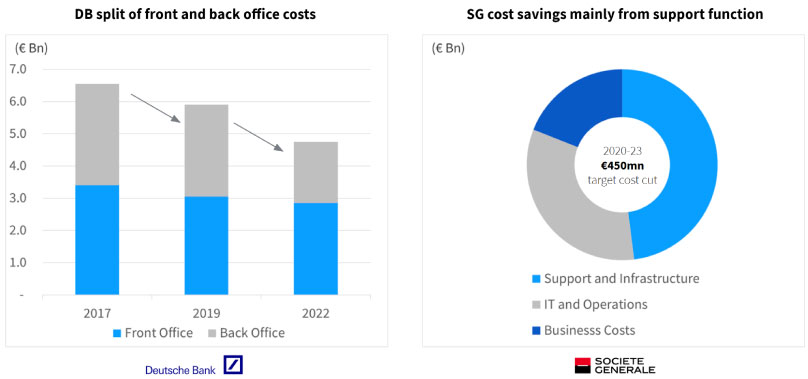

Trend Three: Investing and Cutting spend at the same time

Based on company annual reports, it seems that global banks are also focusing on back-office/support functions, accelerated by the lessons learned from the COVID-19 crisis; i.e., where there are opportunities to scale back on the number of IT help desks, manual compliance monitoring, and other support services which in an environment of work from home were meaningfully less in demand.

For example, Deutsche Bank is in the midst of a major cost restructuring and has indicated that the majority (80%) of cost savings going forward are to come from the back office (figure 3). Societe Generale Group in Global Markets has indicated that its €450mn cost savings from 2022/23 will be driven by support functions while protecting business franchises (figure 2).

Trend Four: Customer data as a differentiator

According to JPMorgan, Global Banks are increasingly looking at ways to utilize technology to offer better services to their clients. Increasing automation/digitalization is also opening areas for further

earnings growth acceleration for Global banks. Notably, customer data can be an enabler to increasing collaboration with other parts of banking. For example, serving both sophisticated Wealth Management clients and corporate banking clients is increasingly crucial for banks to demonstrate a less volatile revenue progression by increasing the share of recurring revenues, which should help lower the cost of equity (CoE).

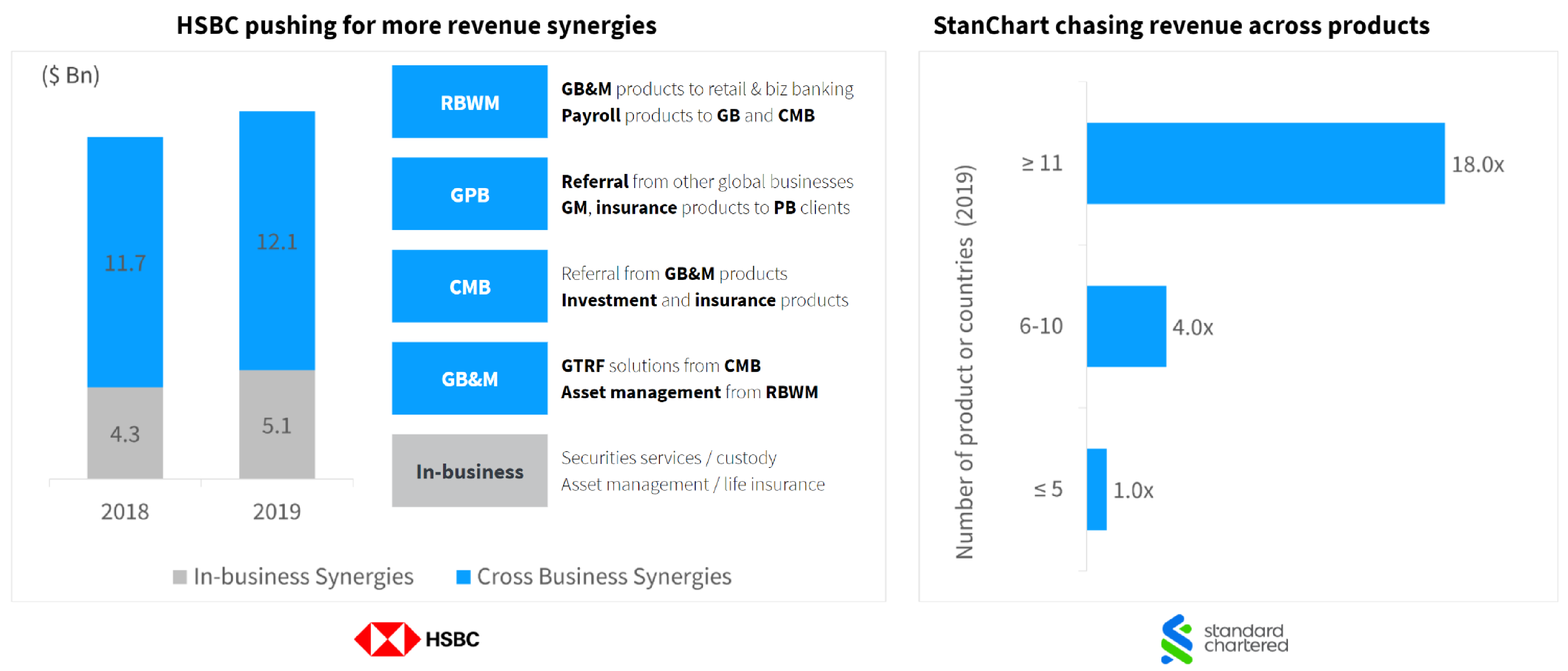

In that spirit, HSBC Group aims to be the global relationship banker to its clients — providing a full range

of banking services ranging from cash management to lending and advisory through the strength of its client relationship. The benefits of this to HSBC are highlighted in their investor presentation about the revenue multiplier effects dependent on the number of products the client utilizes.

Similarly, Standard Chartered Bank says that business units operating across multiple markets also see a multiplier effect on revenues as clients expand their product utilization or bank with StanChart across multiple countries (figure 4). Offering products across different business units also provide banks with stickier revenues and drive a lower cost of funding for the Group.

What do these trends say about modern data problems at big banks?

So what does this mean for technology investments going forward? Is there a common need/idea these trends are attempting to solve/improve?

As many of the banks noted in their strategic initiative, solving the problem of “no single, authoritative source of client data” or “rolling out a single source for reference data” is a critical measurement in the success of their data strategy. Banks like HSBC and StanChart need to activate the customer data they’re collecting to drive revenue to achieve revenue synergies between business divisions.

In other words, they need mastered customer data to be continuously ‘live’ and up-to-date and can be fed to operational and analytical systems to drive business outcomes.

The original article by Qin Li from Tamr is here.

The views and opinions expressed in this article are those of the author and do not necessarily reflect those of CDOTrends. Image credit: iStockphoto/sarayut; Graphs: Tamr